It seems generally agreed that today's troubles in the sub-prime lending area were triggered by two factors: declining home prices and lousy lending standards.

Flat or declining prices closed off the "escape route" of refinancing for many buyers whose payments were ready to "reset," meaning the expiration of a low…

It seems generally agreed that today's troubles in the sub-prime lending area were triggered by two factors: declining home prices and lousy lending standards.

Flat or declining prices closed off the "escape route" of refinancing for many buyers whose payments were ready to "reset," meaning the expiration of a low "teaser" rate of 1% to 4% and/or the end of an interest-only or neg-am period.

When the payments jumped, many stopped making payments outright. About 30 seconds later, 40-plus sub-prime lenders went out of business.

(Today's vivid illustration: Two weeks before Opening Day, the Texas Rangers have dropped Ameriquest from the name of their baseball stadium. In a fitting irony, the lender signed a 30-year deal in 2004, but now could no longer make the payments.)

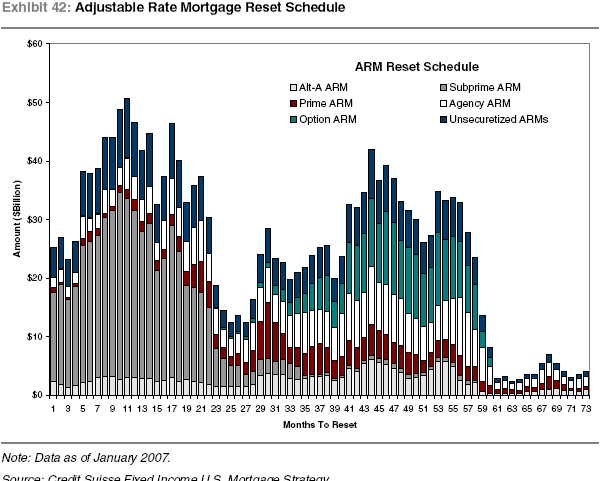

Trouble in the sub-prime area should continue for many months to come, if we look at the dollar volume of sub-prime loans facing reset. (This chart [click to enlarge] is sourced to Credit Suisse, and comes courtesy of a poster at

Mortgage Lender Implode-o-Meter. MBC has made no independent effort to confirm it, or judge its scope.)

How does the sub-prime flameout affect Manhattan Beach?

How does the sub-prime flameout affect Manhattan Beach? Instinctively most people will say there is zero or limited impact. There are no sub-prime buyers in town, you might hear – this is just a different market segment. And the counterargument is that prices everywhere will be negatively impacted, because rot at the "bottom" of the market invariably drags prices at the top, too, with fewer first-time buyers and move-up buyers able to enter the market. This debate sounds a bit indirect and esoteric, however, and it could take years to settle it.

MBC is wondering about another factor:

Loan resets on those million-dollar mortgages held by Manhattan Beach homeowners.All over town, people who bought (or refied) in the last 4-5 years are sitting on adjustable-rate loans with 3- and 5-year "rate lock" periods and interest-only periods. (In MB, these are more likely to be "Alt-A" type or "prime" ARMs, similar in form to many of the subprime loans now going bad.) These "affordability products" were absolutely vital to allowing regular old upper-mid families to buy in during the boom.

Here's the problem. Often, the rate lock and I/O period on these loans will end simultaneously. If you're still holding the loan, you're in a for a payment shock. The only question is how bad it will be.

People who worried about these payment shocks after taking the loans simply told themselves they could always refinance and reset the clock with a new 3- or 5-year I/O period. But if home prices continue flattening or declining, maybe no refi is possible. Your LTV ratio might have gotten worse since you bought.

The next step for the homeowner in this situation is one of three things: 1) Pay the higher payment, perhaps $1,500-$3,000 more per month; 2) Stop making payments and skid along to foreclosure; 3) Sell if you can. It is obvious that more "must-sell" inventory would drag prices down in MB even in the absence of any other factors.

If we're going to see this effect in MB, the chart above suggests that the problems really start about 26-30 months from now (March-June 2009). That's when "prime ARM" resets start to swell. Over the next year or so after, if we're making the right assumptions here, the impact of the resets on homeowners translates into more sellers in trouble and willing to deal.

No less an authority than Alan Greenspan

said just last week that all of these sub-prime problems would "disappear" if home prices simply went up 10%. But wishes aren't fishes. If prices don't go up, a downward trend could accelerate in 2-3 years even in our lovely, luxury beach hamlet.

Note that this discussion ignores the issue of short sales. We don't have short sales in Manhattan Beach!

Please see our blog disclaimer.

Listings presented above are supplied via the MLS and are brokered by a variety of agents and firms, not Dave Fratello or Edge Real Estate Agency, unless so stated with the listing. Images and links to properties above lead to a full MLS display of information, including home details, lot size, all photos, and listing broker and agent information and contact information.