Two problems with adjustable-rate mortgages (ARMs) began the mortgage meltdown earlier this year: rate resets and payment "recasts."

Resets are simple enough to understand: a low interest rate (sometimes an ultra-low teaser rate) expires, and homeowners' payments shift to an adjustable rate, typically higher. That's…

Two problems with adjustable-rate mortgages (ARMs) began the mortgage meltdown earlier this year: rate resets and payment "recasts."

Resets are simple enough to understand: a low interest rate (sometimes an ultra-low teaser rate) expires, and homeowners' payments shift to an adjustable rate, typically higher. That's one payment shock.

Payment "recasts" often occur at the same time – when the "interest only" period on the loan expires, the homeowner must begin to make fully amortized payments. This can boost the monthly payment by 15% or more.

So, this year's meltdown began with resets and recasts on a whole lot of recently issued "subprime" mortgages. Unable to refinance and unable to afford their new payments, many new homeowners stopped paying at all.

The big question for MB and other non-subprime markets is:

When do the loans in our neighborhood start resetting/recasting, and then, what do the homeowners do in response? MBC visited this subject a while back

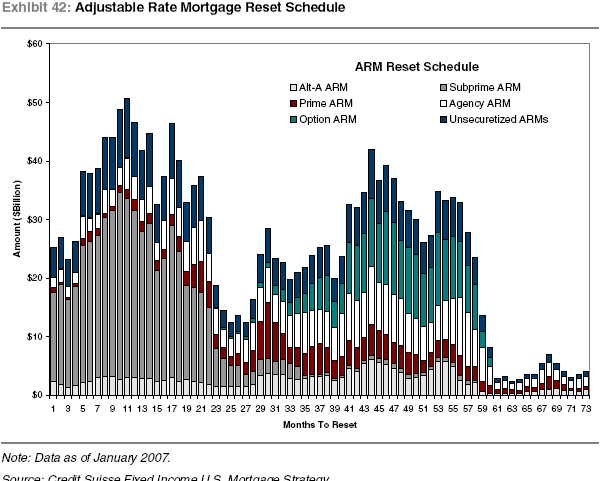

MBC visited this subject a while back, when Credit Suisse published one chart

(right; click to enlarge) showing the resets upcoming over the next 6 years. (

Click here to download the whole Credit Suisse report [PDF].)

Our conclusion then: If there's going to be trouble from resets, it starts in 2-3 years.By Spring 2009, the number of "Prime ARMs" resetting each month nationwide gets big. Presumably that means the phenomenon becomes more common in MB then, too.

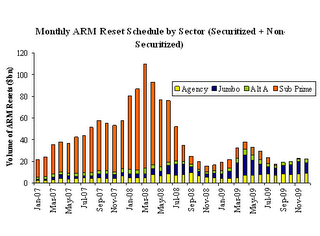

A new chart

(click to enlarge) by a Bank of America analyst,

published Wednesday at Calculated Risk – one of our favorite housing & economics blogs –

largely agrees with that conclusion on timing.

(Nerdy notes: If you compare these, note the different scales – the new chart goes up to $120b, while the older, longer-term chart goes up to just $60b. Also, BofA includes non-securitized loans.) BofA's chart says that a surge in "Jumbo" and "Alt A" resets begins in earnest in

March 2009. That would reflect 3-year locks from 2006 purchases as well as 5-year locks from 2004.

All over MB, people who can actually afford the amortized payments are making I/O payments. They'd like to refinance at some point, but it's not urgent. Others who

can't really afford the amortized payments may need to refi to avoid the payment shocks.

But today you have to worry that the refi option won't be available. Whether it's the credit crunch, interest rates (in '09), your initial LTV, or the LTV in 2009 if the market declines, there might be no refi "safety valve." If that storm comes together, it could mean more forced sales, and presumably lower prices.

(Did you notice the ifs?)This is a long way of saying that most of the recent crop of MB buyers got better terms –

especially longer locks – than the subprime buyers who are now in so much trouble, and all over the news. But when the locks expire here in droves, even upper-income homeowners could feel a lot of pressure.

We'd be remiss not to mention the screaming headline from the BofA graph.

Look at the orange bar in Jan. 2007. Those subprime resets were just taking off as the mortgage meltdown began. Now look at Jan. 2008, and March 2008, and beyond. That orange bar swells up nastily.

You think the "subprime debacle" is big news today? What happens 3-9 months from now?

Please see our blog disclaimer.

Listings presented above are supplied via the MLS and are brokered by a variety of agents and firms, not Dave Fratello or Edge Real Estate Agency, unless so stated with the listing. Images and links to properties above lead to a full MLS display of information, including home details, lot size, all photos, and listing broker and agent information and contact information.

Based on information from California Regional Multiple Listing Service, Inc. as of July 26th, 2024 at 10:19pm PDT. This information is for your personal, non-commercial use and may not be used for any purpose other than to identify prospective properties you may be interested in purchasing. Display of MLS data is usually deemed reliable but is NOT guaranteed accurate by the MLS. Buyers are responsible for verifying the accuracy of all information and should investigate the data themselves or retain appropriate professionals. Information from sources other than the Listing Agent may have been included in the MLS data. Unless otherwise specified in writing, Broker/Agent has not and will not verify any information obtained from other sources. The Broker/Agent providing the information contained herein may or may not have been the Listing and/or Selling Agent.