Let's start out here by giving credit where it's due – no, wait, unfortunate phrasing... there's been too much credit out there for a while.

Let's congratulate our elected leaders and the quasi-governmental overlords of our financial system. They know that the storm is only just getting started, and they are trying…

Let's start out here by giving credit where it's due –

no, wait, unfortunate phrasing... there's been too much credit out there for a while.

Let's

congratulate our elected leaders and the quasi-governmental overlords of our financial system. They know that the storm is only just getting started, and they are trying to get some pieces in place to get the public ready and set up emergency services, just in case the storm hits hard. "Subprime," they know now, was like the whipping winds at the leading edge of a storm that looks to be on the horizon. No sense spinning the story now.

We'll check in here with the Treasury Secretary, the Fed and the U.S. Congress. They're all trying to help.

Paulson and the 'Hope Now Alliance'Here's Henry Paulson, former Goldman Sachs CEO and current U.S. Treasury Secretary, at Tuesday's news conference, responding to a reporter's question:

Q: Sir, is the worst over? Will 2008 have fewer foreclosures and some rising home prices, compared to '07?

Paulson: Well, I would say this, in terms of subprime, and the resets, the worst isn't over, it's just beginning. We all know that.

Paulson: Well, I would say this, in terms of subprime, and the resets, the worst isn't over, it's just beginning. We all know that.

There's close to 1.8 million, 2 million adjustable rate mortgages where the rate is going to be reset, and the ones that are being reset over the next couple of years are that vintage of mortgages where there were the most lax underwriting procedures. So, this is the biggest challenge. That's why this is so important.

And I also said that the housing correction – what's going on with the housing market – is not over. It's going to take longer.

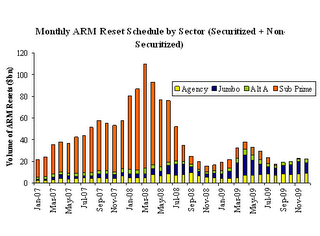

Paulson must know that his old firm now projects March 2008 as "the worst" month for subprime resets, with plenty of other nontraditional loan products expected to go bad on their own schedules through 2010. (Consistent with this BofA chart

we published in Aug. 2007 [

click to enlarge].) Of course, the impacts of resets (defaults, foreclosures, REOs, losses & writedowns) follow over several months afterward.

Quick tangent – if you think securitized residential mortgages were a kick in the arse, Goldman warns, get ready for flareups among securitized

commercial mortgages next. Frightening fact, via Goldman: whereas about 20% of commercial RE loans were interest-only in 2000, that share rose to 86% of those issued in 2007. Can you say "increased default risk?" Now, who holds those loans in bulk?

Back to Hank. The cause for Paulson's news conference Tuesday was to announce a new "lifeline" that 6 major banks will offer to home loan borrowers in default. Here's how it works:

In an effort to get the attention of defaulting borrowers, the banks will send them a letter. Really.

A letter – that was the point of the news conference. (If you think we're diminishing the real program, click here for

the press release or here for the

"overview" of "Project Lifeline.")

Borrowers who get the letter need to call the lender within 10 days, profess a desire to keep their home, and supply financial information so the bank can assess what kind of a workout is possible. If foreclosure is under way, the banks might pause it for 30 days.

This is not much of a rescue plan. In fact, it is pointedly not a "moratorium on foreclosures," the materials note. (Certain presidential candidates have demanded that.)

Paulson and the 6 banks (the "Hope Now Alliance") were criticized for ignoring defaulting homeowners with The Freeze, a plan announced in December to put off rate resets for certain deserving borrowers. (See MBC's "

The Freeze & The Hope.") So this is the bone they're throwing –

oh, sorry, "lifeline" – to the bad-news borrowers.

Now they've got 2 press conferences and 2 plans that might help a little portion of the people whose loans are going bad.

They're trying. We can't say they're really doing much.

MBC is especially skeptical of the new plan because folks in default have often made a psychic break long before the first Notice of Default arrives. By the time the bank calls or sends a letter, the borrowers are hearing from all sorts of would-be rescuers (foreclosure sharks, mainly) and they can be immune to the sort of "hope" this "lifeline" plan is supposed to offer.

The best that can be said for all this hype from "Hope Now" is that it

might help to reach a few more borrowers in trouble, and inspire them to work with their lenders. On a case-by-case basis, that matters, but it doesn't change the fundamentals much.

The FedSome of the other big news out of D.C. is the Fed's ongoing rate-cutting campaign.

(Thank you, sirs, may we have another?) The market expects another 0.5% cut at the next meeting, and that would put the Fed's rate inarguably below the rate of inflation.

The Fed cuts are having all sorts of impacts, but they're not affecting rates on new mortgages much. (Some borrowers with adjustable-rate loans will benefit.) As is painfully apparent, mortgage rates are driven by other factors – long-term notes and inflation expectations among them.

In a worst case, the Fed's efforts to stimulate the economy with easier credit cause price inflation and higher mortgage rates, making home-buying even less affordable. The result would be

downward pressure on home prices. That's OK if the Fed doesn't care about the housing market, per se, but it is clearly reacting now to the ripple effects of declining house prices.

Do you get a better result by tamping down home prices further?Back to Paulson for a moment. As we noted

in a recent story, the Treasury Sec'y believes that the "housing correction is

inevitable and necessary." We'll take that as his vote for tamping down home prices further.

The U.S. CongressA new economic stimulus package passed by Congress has a critical housing-related provision. The GSEs (Fannie Mae, Freddie Mac) will be able to buy much bigger loans – up to $730k for loans issued in the

second half of this year (July 1 '08-Dec. 31 '08). That's up from $417k.

The move will redefine "jumbo" loans this Summer as those loans over $730k. Buyers who need less – at least for a 1st TD – should have readier access to home loans than they do under today's regime of skittish lenders and nonexistent secondary-market buyers (for packaged mortgages).

Translation: Come Summer, it might be easier to get a loan than it is now.

But a lot depends.

There's fear that rates will increase across the board, even for lower-level borrowers, to account for the risk of higher-priced, GSE-targeted loans.

No question these new loans will reflect tougher standards than private lenders have recently begun to adopt. You'll need great income and LTV ratios to get a benefit here.

It seems to MBC that, with so much of the recent housing market runup being tied to lax lending standards (see Paulson, way above), tougher standards

plus a declining-price environment translate rather naturally to the need for a broader and deeper drop in home prices. Potential buyers can only tap the promised stream of new liquidity if they can truly afford the homes they're purchasing.

In the end, the actions by Hope Now, the Fed and the Congress all sound like efforts to fix the housing market and stabilize prices, but not one of them provides a clear path to do so. Indeed, both Paulson and the Fed seem to be selling out the housing market in favor of bigger concerns. Let's see what that storm really looks like. Batten down the hatches, just in case.