It's comforting to think that the headlines about sub-prime loans and foreclosures simply don't mean anything for Manhattan Beach real estate.

Comforting, but not completely true.

First, the news: Today's LA Times business section features a front-page story, "Foreclosure pace nears decade high," much gloomier than…

It's comforting to think that the headlines about sub-prime loans and foreclosures

simply don't mean anything for Manhattan Beach real estate.

Comforting, but not completely true.

First, the news: Today's LA Times business section features a front-page story, "

Foreclosure pace nears decade high," much gloomier than the typical LA Times real estate story.

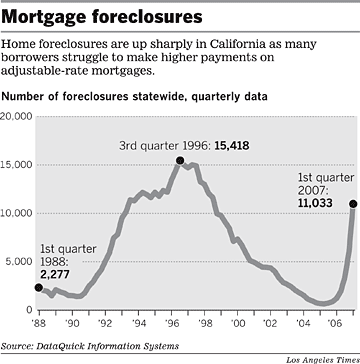

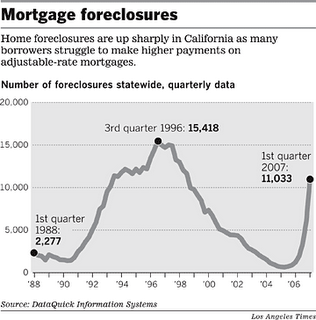

There are now 900 homeowners per week losing their homes in California to foreclosure, up from 100 per week one year ago. More than 11,000 foreclosures in the first three months of 2007 represented an 800% increase over the same period last year. Cue the housing bear:

"For this rise in foreclosures to be happening in the midst of a strong labor market is truly unique and scary," said analyst Christopher Thornberg of Beacon Economics.

Incredibly, Thornberg predicts a four- to five-fold increase in foreclosures.

A chart provided by the Times suggests that Thornberg expects foreclosures at triple the peak reached in 1996 (15,418). What if he's only half right?

The article goes on to discuss how foreclosures are concentrated in "the places with the cheapest housing in the state," with San Diego County as a notable exception – "the county's market peaked earlier than the rest of the state."

Whose loans are going into foreclosure? "Most of the loans," says the Times, "going into default now were made at the peak of the housing boom in 2005."

MBC offers a local example. On the market today, you'll find

601 Larsson, a nice Hill Section remodel, 4 bed, 4 bath, almost 4,000 square feet. Purchased in Sept. 2005 for $2.0m, now listed at $2.499 after starting (March 20) at $2.695.

601 Larsson goes to public auction May 4 if no one buys it real, real soon. Not that you'd know from the listing language – no reference to the legal troubles.

Also, the Beach Reporter carried a legal notice last week that

958 Rosecrans would go up for auction tomorrow, April 18. This 2 bed/1 bath, 975 sq. ft. house was purchased July 3, 2006, for $977,500. The note gone bad was worth over $800k.

Who loses a house in less than a year?Also coming up for auction May 4 –

225 39th St., just a door down from Highland Ave. in El Porto. No recent purchase here, but records indicate a $1.005m loan gone bad.

HELOC hell? Zillow thinks the property is worth $982k, less than the loan. Minimum bid is $1.1m. Uh-oh.

Another active listing in default:

2816 Manhattan Ave. This is new construction first listed in Sept. 2006. However, it appears to be an old loan that went bad. Surely this can be fixed before auction, but the process must be stressful for the builder. Why, then, has there never been a price reduction after 7 months on market at $2.9m?

Overall, according to one source, there are just 4 homes in 90266 now in foreclosure, and 15 more in default. Not bad for a pretty big town with some very, very big mortgages. Let's hope this remains a rare phenomenon.

Please see our blog disclaimer.

Listings presented above are supplied via the MLS and are brokered by a variety of agents and firms, not Dave Fratello or Edge Real Estate Agency, unless so stated with the listing. Images and links to properties above lead to a full MLS display of information, including home details, lot size, all photos, and listing broker and agent information and contact information.