How New Tax Law Might Hit Manhattan Beach

When the 2016 election put a real estate developer into the White House, who would have bet we'd get legislation to harm homeowners and home builders? Well, it's a strange year.

As they work in Washington, D.C., to iron out final details of Senate and House-passed versions of tax law changes, only one thing is…

As they work in Washington, D.C., to iron out final details of Senate and House-passed versions of tax law changes, only one thing is…

Some of Our Content is for Registered Users Only

Unlock PostWhen the 2016 election put a real estate developer into the White House, who would have bet we'd get legislation to harm homeowners and home builders? Well, it's a strange year.

As they work in Washington, D.C., to iron out final details of Senate and House-passed versions of tax law changes, only one thing is really clear: These tax law changes will create uncertainties and challenges for the real estate market everywhere. Many fear the worst.

Homes and homeowners in pricey coastal markets like Manhattan Beach could take an especially rude punch from the new tax legislation. From here, the bills sure look like a package of property-related tax increases.

Here's what we know now about the tax bills passed in each chamber:

Over $10K in Property Tax No Longer Deductible

This could be a body blow to many homeowners and home buyers in our area. Almost overnight, the deductibility of property tax would be capped at $10,000 per year. (That figure would not be indexed, meaning it becomes less valuable over time with inflation.)

This would mean immediate increases in many local families' housing-related costs. On a home assessed at $2.000M (about the median price of recent sales in Manhattan Beach), this would mean an increase of almost $12,000 per year. On a $3.000M house, it's almost $23,000. And so on. (Here's our page on Manhattan Beach property taxes.)

This is just a piece of the impact of the tax bills' elimination of deductions for state & local taxes. It's likely the biggest impact tied to real estate for Manhattan Beach residents.

(Note: The alternative minimum tax [AMT] in current law may already limit the benefit of property tax writeoffs for some taxpayers locally. Here we have to generalize the impact. The House bill drops the AMT, but the Senate bill keeps it, with changes.)

More Time Required in a Home for Capital Gains Exclusion

Currently, a portion of capital gains from sale of a personal residence can be exempt from tax. That's $250,000 for an individual or $500,000 for a couple.

Today, to get the exemption, you must have lived in the home for 2 of the prior 5 years.

The tax law changes passed by both the House and Senate will require living 5 of the prior 8 years in the home, and there may be new "income limits" applying to further curtail who could claim the exemption. (Sorry, we don't have those proposed "limits" yet, still researching.)

In addition, the capital gains exclusion could be used only once every 5 years, instead every 2 years currently.

Mortgage Interest Deduction May Be Limited (Primary Residence)

The mortgage interest deduction (MID) of greatest interest to Manhattan Beach is still in play.

The mortgage interest deduction (MID) of greatest interest to Manhattan Beach is still in play.

Current law allows a tax deduction for interest paid on up to $1.000M of mortgage financing. (For taxpayers who itemize.) The House cut the deduction to interest on only $500K, but the Senate brought it back to $1.000M. The difference must be settled in conference.

The MID was already being called endangered or irrelevant as it applies to mortgages only up to $500K. That's because a main part of the tax bills would aim to eliminate almost all deductions, by nearly doubling the standard deductions.

Nationally, it's projected that almost all taxpaying homeowners would take the doubled standard deduction and not itemize. Renters and homeowners, then, would get largely the same writeoffs. If few claim the MID, it ceases to be an extra incentive for homeownership.

In Manhattan Beach and other parts of the South Bay, a new purchase with a mortgage of $500K-$1M or more is common. So if that higher, current $1M cap remains (after conference), new local buyers might have pretty much the same MID-related incentives here as recent buyers. Indeed, nationally, the MID might become a benefit that is mostly claimed for mortgages of $500K-$1.000M. Watch the conference results on this topic.

Mortgage Interest Deduction Ended for Second Homes, Home Equity Loans

Under the House bill, there would no longer be an option to deduct mortgage interest from second homes. The Senate preserved the current deduction, putting the issue to conference.

In addition, no interest on home equity loans would be deductible. The House bill would apply this new rule only to new home equity loans, while the Senate bill would end deductibility immediately for existing loans also. The discrepancy goes to conference.

Lower Tax Rate for Rental Income

What's this? Good news?

The House bill would reduce the top tax rate on rental income to 25%, down from a max of 39.6% today.

The Senate took a different approach for landlords raking in $700K or more in rent annually, keeping top tax rates in place unless the landlord has a threshold number of employees and expenses. There are differences to resolve in conference.

In addition, one report states that the Senate would allow mortgage interest on rental properties to be deducted in full. That's an issue to watch as the final bill is resolved.

What Does It All Mean?

Let's be clear: That is not an attractive or welcome set of changes.

You could pay more tax on 3-4 real estate-related fronts than you would today.

You could pay more tax on 3-4 real estate-related fronts than you would today.

The cost of owning a home will go up. Potential sellers will have to think twice before going to market if they were planning on a capital-gains exemption. Do they qualify? What does that do to inventory, or sellers' pricing?

Buyers are going to expect to take a pound of flesh out of asking prices to account for their higher costs. The stage is set for some tough negotiations.

Nationally, projections are that the tax bills would reduce home prices by at least 5% (Moody's) or more. The National Association of Realtors projects the impact at 8-12% for California, worrying about "a plunge in home values across America in excess of 10 percent, and likely more in higher cost areas."

"More in higher cost areas." Uh-oh.

Yes, that's the "voice for real estate" telling everyone prices will drop substantially. (We've added more choice quotes from NAR below, in case you'd like to see what it sounds like when the volume on these worries is turned up to 11.)

A Sensitive Time for Manhattan Beach Real Estate

Way-back-when there was a housing bubble. It wiggled and wobbled in 2007-08 and popped in 2008-09. Manhattan Beach prices dropped 18-20% over a couple of years.

Way-back-when there was a housing bubble. It wiggled and wobbled in 2007-08 and popped in 2008-09. Manhattan Beach prices dropped 18-20% over a couple of years.

Home sales volume and prices in Manhattan Beach bounced back from 2010-2017, with the greatest rally in prices occurring roughly from 2013-15. Prices are higher now than ever. The number of homes sold in Manhattan Beach this year is higher than in any of the last 4 years.

Still, you could call this time now a "moment of uncertainty" in the Manhattan Beach real estate market - before the tax bill was passed.

It's not really a time when you would want to try something new, especially something new that seems to have little upside for local real estate.

Individual high-net-worth or high-income homeowners and home buyers may or may not end up worse off, on balance, from the whole mix of tax law changes, but the tax-related incentives and benefits of home buying seem to be taking a hit. The reasons to buy homes - there are plenty - will have to stand apart from the notion of getting super tax benefits.

Maybe you are thinking, "If only we could get the word out! This could be stopped!"

Maybe, but it sure seems that the authors of these tax bills meant to target certain high-cost states and real estate markets. Only 3 of 14 California Republicans voted against the bill in the House.

Maybe, but it sure seems that the authors of these tax bills meant to target certain high-cost states and real estate markets. Only 3 of 14 California Republicans voted against the bill in the House.

Harm to Manhattan Beach real estate - if it occurs - would not be a bug, but a feature of the tax bill.

Sometimes when a tax goes up, like, say, a cigarette tax devoted to smoking prevention, you can rationalize the higher cost by saying, "At least that money's going to a good purpose."

So perhaps we should take some time to appreciate all the benefits of the new tax bills, too.

OK, done. Do you need more time?

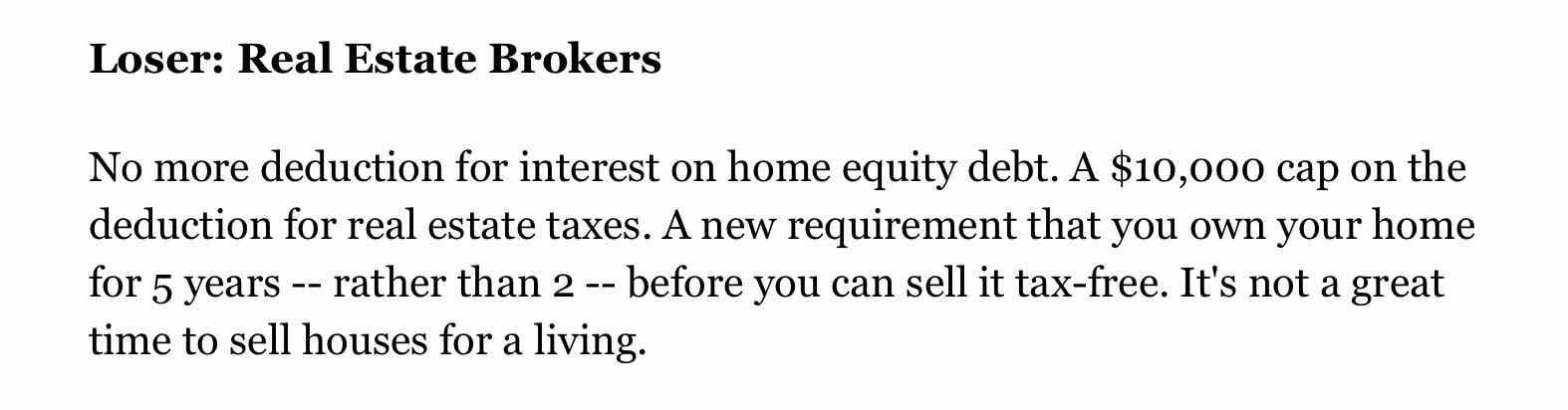

Impact on Real Estate Business

Do you care about the local real estate market or brokers more? Haha, trick question.

One Forbes magazine writeup on the tax law changes put the impact for brokers pretty bluntly.

One Forbes magazine writeup on the tax law changes put the impact for brokers pretty bluntly.

With the tax changes taking effect: "It's not a great time to sell houses for a living."

Gee, thanks.

It's Not Over Till It's Over

As we noted above, competing versions of the tax law changes have to be worked out between the House and Senate versions. You can see from our summary that there are significant choices to be made affecting real estate.

And the final bill does need to be signed by the occupant of the White House. A foregone conclusion, perhaps, given all the cheerleading for the bill, but it is not really done till it's done.

And the final bill does need to be signed by the occupant of the White House. A foregone conclusion, perhaps, given all the cheerleading for the bill, but it is not really done till it's done.

The realtors' lobby is targeting two issues: 1) keeping the $1M mortgage interest cap and 2) returning the capital gains exemption ($250K/$500K) to a 2-of-5 cycle rather than the new 5-of-8 requirement. We'll see what they can do.

A silver lining from all this?

Don't look for mortgage rates to spike if new tax law changes threaten the housing market. Cheap money has flowed for several years, and it's the only remedy monetary authorities have to try to contain the damage if worst-case scenarios begin to play out in real estate markets.

We'll report back on the final bill if/when it's signed and check in on these and other issues in a final scorecard.

QUESTIONS? CONCERNS? CORRECTIONS?

This is a blog. We've done our best to capture the current info on bills that not everyone has read or had full access to so far.

We welcome feedback and will make changes where needed.

Please just email Dave directly if you don't want to comment on the blog here.

–––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––––

Bonus Addendum

NAR's Strong Rhetoric of Warning

NAR's Strong Rhetoric of Warning

You ought to know that lobbyists and campaigners can be pretty strident when advocating for their positions.

If you listen to the national real estate lobbies (realtors & builders), with these tax bills, we are facing a kind of Armageddon. Very recent statements by the National Association of Realtors on the tax bills:

• "for tax purposes, owning a home would make less financial sense than renting for the great majority of Americans"

• the bills "would destroy or at least cripple the incentive value of the mortgage interest deduction... and sap the incentive value of the property tax deduction for millions more"

• "The hard-won equity of millions more homeowners could be ravaged"

• "millions of middle-class homeowners would immediately face tax increases, while those who see a tax cut will see significantly less tax relief if they own a home than if they are a renter."

• "The direct result of these changes would be a plunge in home values across America in excess of 10 percent, and likely more in higher cost areas."

• the tax law changes "would change the face of homeownership in this country for decades to come"

And this from NAR President Elizabeth Mendenhall immediately after the Senate vote:

“The tax incentives to own a home are baked into the overall value of homes in every state and territory across the country. When those incentives are nullified in the way this bill provides, our estimates show that home values stand to fall by an average of more than 10 percent, and even greater in high-cost areas. Realtors support tax cuts when done in a fiscally responsible way; while there are some winners in this legislation, millions of middle-class homeowners would see very limited benefits, and many will even see a tax increase. In exchange for that, they’ll also see much or all of their home equity evaporate as $1.5 trillion is added to the national debt and piled onto the backs of their children and grandchildren."

Surely NAR is fighting a mighty endgame, but the biggest changes seem baked into the bills.

Please see our blog disclaimer.

Listings presented above are supplied via the MLS and are brokered by a variety of agents and firms, not Dave Fratello or Edge Real Estate Agency, unless so stated with the listing. Images and links to properties above lead to a full MLS display of information, including home details, lot size, all photos, and listing broker and agent information and contact information.

Based on information from California Regional Multiple Listing Service, Inc. as of April 27th, 2024 at 5:45pm PDT. This information is for your personal, non-commercial use and may not be used for any purpose other than to identify prospective properties you may be interested in purchasing. Display of MLS data is usually deemed reliable but is NOT guaranteed accurate by the MLS. Buyers are responsible for verifying the accuracy of all information and should investigate the data themselves or retain appropriate professionals. Information from sources other than the Listing Agent may have been included in the MLS data. Unless otherwise specified in writing, Broker/Agent has not and will not verify any information obtained from other sources. The Broker/Agent providing the information contained herein may or may not have been the Listing and/or Selling Agent.